Why a correct invoice is important

A professional invoice is much more than a payment receipt - it is the legal basis of your payment claim. Without a correct invoice, your customer can refuse payment and the tax office will not recognise the input tax deduction. For the self-employed, freelancers and entrepreneurs, this issue is therefore of existential importance.

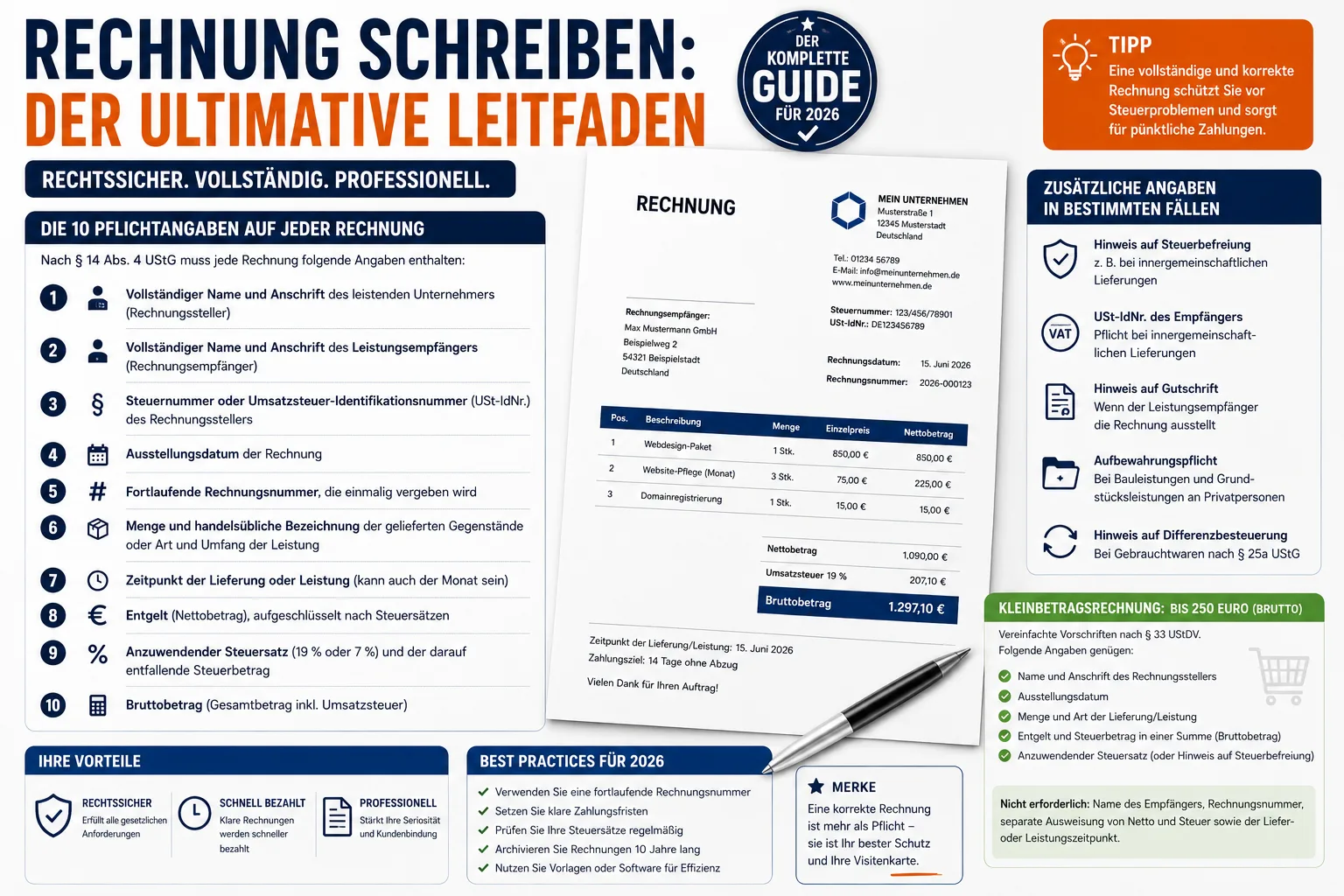

In Germany, § 14 UStG (Value Added Tax Act) regulates what information an invoice must contain. If even one mandatory item is missing, the invoice is formally incorrect - with potentially expensive consequences in the event of a tax audit. In this case, the tax office can cancel the recipient's input tax deduction, which can lead to considerable additional payments.

In addition, a clean, professional invoice signals seriousness and reliability to your business partners. It speeds up the payment process and reduces queries. If you regularly send out incorrect invoices, you not only risk financial losses, but also a loss of reputation.

The 10 mandatory details on every invoice

According to § 14 para. 4 UStG, every invoice must contain the following information:

- Full name and address of the supplier (invoicing party)

- Full name and address of the recipient of the service (invoice recipient)

- Tax number or VAT identification number (VAT ID no.) of the invoicing party

- Date of issue of the invoice

5 Consecutive invoice number, which is assigned once

- Quantity and commercial description of the delivered goods or type and scope of the service

7 Time of delivery or service (can also be the month)

- Compensation (net amount), itemised according to tax rates

- Tax rate to be applied (19% or 7%) and the tax amount attributable to it

- Gross amount (total amount incl. VAT)

Additional information in certain cases

- Note on tax exemption: In the case of tax-free services (e.g. intra-Community deliveries), a corresponding reference must be made, e.g. "Tax-free intra-Community delivery according to § 4 No. 1b i. V. m. § 6a UStG"

- VAT ID number of the recipient**: For intra-Community deliveries, the VAT ID no. of both parties is mandatory

- Reference to credit note: If the recipient of the service issues the invoice (credit note procedure), the word "credit note" must appear on the document

- Obligation to keep records**: For certain construction services and property services to private individuals, reference must be made to the 2-year retention obligation

- Note on differential taxation: For used goods according to § 25a UStG, a reference to the differential taxation must be made

Small value invoice: Simplified rules up to 250 euros

For invoices up to a total amount of 250 euros (gross), simplified rules apply in accordance with § 33 UStDV. This typically applies to cash receipts, petrol receipts or small service invoices. The following information is sufficient:

- Name and address of the invoicing party

- Date of issue

- Quantity and type of delivery/service

- Remuneration and tax amount in one sum (gross amount)

- Applicable tax rate (or reference to tax exemption)

Not required for low-value invoices: Name of the recipient, invoice number, separate statement of net and tax as well as the time of delivery or service.

Practical tip:** Even if it is not mandatory, you should still include an invoice number. This makes your own bookkeeping considerably easier and prevents chaos when allocating invoices.

Small business regulation according to § 19 UStG

Anyone who did not generate more than 25,000 euros in turnover in the previous year and is expected to generate not more than 100,000 euros in the current year can make use of the small business regulation. This regulation was reformed on 1 January 2025 - the previous limits were 22,000 euros and 50,000 euros.

What this means in concrete terms:

- You do not show any VAT** on your invoices

- You do not pay VAT to the tax office

- The monthly or quarterly advance VAT return is omitted

- In return, you cannot claim any input tax deduction - VAT on purchases remains your cost burden

- A reference to § 19 UStG must be included on every invoice

Example wording for the note:

- "According to § 19 UStG no sales tax will be charged. "

- "No VAT will be charged due to the application of the small business regulation according to § 19 UStG".

Important: If you forget the note on the invoice, you still owe the VAT - because the invoice recipient can then deduct it as input tax (§ 14c UStG). This error can be expensive and can only be rectified by correcting the invoice.

Assign consecutive invoice numbers correctly

The invoice number must be unique - this is the only mandatory requirement of the law. Contrary to a widespread misconception, it does not have to be continuous. The Federal Fiscal Court (BFH) has confirmed this several times. Gaps in the numbering are not grounds for objection.

Proven formats:

RE-2026-0001(prefix + year + consecutive number)2026-03-001(year + month + number)F-0001(single consecutive with letter prefix)

You can also use different number ranges - e.g. one for domestic invoices and one for foreign invoices, or separated by business area. It is only important that no number occurs twice within each number range.

Frequent error: Invoice numbers assigned twice. This happens particularly often with manual allocation in Excel or Word. Invoice software** such as Easy Invoice automatically prevents this by assigning numbers consecutively.

Deadlines: When must the invoice be issued?

Invoicing deadline

- B2B services: The invoice must be issued within 6 months** of the performance of the service (§ 14 para. 2 sentence 2 UStG). A fine of up to 5,000 euros may be imposed if the deadline is exceeded.

- B2C services**: No statutory deadline for invoicing, but prompt invoicing is in your own interest

Payment deadlines

- Unless otherwise agreed, the statutory payment period of 30 days applies (Section 286 (3) BGB)

- In the case of consumers (B2C), default only occurs after a reminder, unless a specific date has been specified on the invoice

- For business customers (B2B), default occurs automatically after 30 days - even without a reminder

Retention periods

Invoices must be kept for 10 years (§ 14b UStG). The period begins at the end of the calendar year in which the invoice was issued. An invoice from March 2026 must therefore be kept until 31 December 2036.

Important: This applies to outgoing AND incoming invoices. In the case of digital invoices, machine analysability must be guaranteed - a PDF is sufficient, a screenshot or photo of the invoice is not. The GoBD (principles of proper bookkeeping) stipulate that electronic invoices must be saved in their original format.

E-invoicing: What applies from 2025

As of 1 January 2025, new rules for electronic invoices in the B2B sector will apply in Germany. The changes affect practically all companies:

Timetable for mandatory e-invoicing

| From when | What applies |

|---|---|

| 01.01.2025 | All companies must be able to receive e-invoices |

| 01.01.2027 | Companies with > €800,000 turnover must send e-invoices |

| 01.01.2028 | All companies must send e-invoices |

What is an e-invoice?

An e-invoice is not a PDF by e-mail. It is a machine-readable, structured XML format that can be processed automatically and without media discontinuity. The common formats in Germany are

- XRechnung: Pure XML format, mandatory for invoices to public clients (federal, state and local authorities)

- ZUGFeRD 2.x**: Hybrid format - a PDF/A-3 with embedded XML. Human-readable and machine-processable at the same time. Particularly suitable for SMEs.

Tip:** Check early on whether your invoicing software can create and receive e-invoices in XRechnung or ZUGFeRD format. If you don't take care of this until 2027, you may have a problem.

7 common mistakes when writing invoices

1 Missing tax number or VAT registration number - The most common mistake of all. Without this information, the recipient cannot deduct input tax and your customer will ask you for a correction. 2 Wrong tax rate - 19% and 7% are easily confused. The reduced rate of 7% applies to food, books, magazines, works of art and certain cultural services, among other things. 3 No date of performance stated - Even if the invoice date and the date of performance are identical, this must be noted on the invoice. The simple sentence "Invoice date = service date" is sufficient. 4 Invoice number assigned twice - Happens quickly with manual numbering in Word or Excel. Use software with automatic number assignment. 5 Missing bank details - Although not mandatory under the German VAT Act, without IBAN, BIC and account holder, payment is unnecessarily delayed. Some customers wait until they receive the bank details. 6 Wrong recipient address - Especially for corporate customers with several locations and for groups with centralised invoice acceptance, it is essential to check this. 7 Forgotten small business reference - Without the reference to § 19 UStG, you owe the tax office the VAT shown (or not shown) in accordance with § 14c UStG.

Tips for faster payment

The best invoice is of little use if it is only paid weeks later. With these measures you can speed up the receipt of payment:

- Offer a discount: "We grant a 2% discount for payment within 10 days" is a strong incentive. Many accounting departments are instructed to utilise discount periods.

- Place bank details prominently**: IBAN, BIC and account holder directly below the total amount - not hidden in the footer

- Specify the payment target**: "Payable by 15 April 2026" is clearer than "Payable within 30 days" - the recipient doesn't have to do the maths

- Issue invoice immediately**: The faster the invoice goes out, the faster it will be paid. Ideal: on the same day as the service

- Offer online payment**: PayPal, credit card or direct bank transfer - the easier the payment method, the faster the money arrives

- Automatic payment reminders**: Many invoicing programmes automatically send a friendly reminder after the deadline has passed

Cancelling or correcting an invoice

An invoice that has already been sent may not simply be cancelled or subsequently changed. This would be a violation of the GoBD. There are two correct ways to deal with errors:

Cancellation invoice (credit note)

You create a credit note (cancellation invoice) for the same amount, which completely cancels the incorrect invoice. You then issue a new, correct invoice with a new invoice number. The credit note is also given its own number.

Invoice correction

You refer to the original invoice number and invoice date in a correction document. You then only correct the incorrect details. The original invoice remains in the system.

Important:** Never delete an invoice from your system. Complete and unalterable documentation is required by law under the GoBD. Changes must be logged in a traceable manner.

Digital or paper: which is better?

Digital invoices (e.g. as a PDF by e-mail) are legally fully equivalent to paper invoices. Since 2011, a qualified electronic signature is no longer required in Germany.

Advantages of digital invoices:

- Immediate delivery - no postage, no loss of time

- Lower costs - no postage, no paper, no printing

- Easier archiving - digitally searchable and space-saving

- More environmentally friendly** - less paper consumption and CO₂ by post

- Preparation for the e-invoicing obligation from 2025/2027

Only requirement: The recipient must consent to electronic invoicing. Tacit consent through uncontradicted payment is sufficient in practice.

Frequently asked questions (FAQ)

Do I have to write invoices as a freelancer?

Yes, every entrepreneur within the meaning of the UStG is obliged to issue invoices - including freelancers, self-employed persons and small businesses. The obligation always exists for services to other entrepreneurs (B2B).

Can I issue an invoice without a tax number?

Only if you state your USt-IdNr. instead of your tax number. One of the two numbers is mandatory. Many entrepreneurs prefer the VAT ID number, as the tax number allows conclusions to be drawn about the responsible tax office.

What happens if the invoice is incorrect?

The invoice recipient cannot claim the pre-tax deduction until the invoice is corrected. In the worst case, a tax audit could result in back payments plus 6% interest per year on the back payment amount.

How long do I have to keep invoices?

10 years from the end of the year of issue - for both outgoing and incoming invoices. In some cases, even longer periods apply to property and land.

Does an invoice have to be signed?

**No. A signature has no longer been mandatory on invoices since 2004. However, it can strengthen the recipient's trust.

What language must the invoice be in?

There is no legal requirement regarding the language. The invoice may be issued in any language. However, the tax office may require a German translation if it wishes to check the invoice.

Create professional invoices with Easy Invoice

With Easy Invoice you can create legally compliant invoices in just a few clicks - with all mandatory information, automatic invoice numbering and a professional layout. Whether you are a sole trader or a growing team: your invoices are always correct and legally compliant.

- All mandatory information according to § 14 UStG automatically included

- Consecutive invoice numbers** - no duplicates, no gaps

- Small business mode with automatic § 19 UStG reference

- PDF export** and dispatch directly from the application

- 10 years of GoBD-compliant archiving** in the cloud

- Multilingual invoices** for international business partners

- Prepared for the E-invoice obligation (XRechnung and ZUGFeRD)

Handle invoices more easily

Easy Invoice combines quotes, invoices and customer management in the cloud.

Try Easy InvoiceRead next

Invoicing & Accounting

Invoicing & Accounting

ZUGFeRD 2.5 from 1 July 2026: What changes for your invoices

ZUGFeRD 2.5 has been available since 10 June 2026 and should be used from 1 July. What actually changes, who the e-invoice applies to at all, and why up-to-date software keeps things stress-free.

Invoicing & Accounting

Invoicing & Accounting

Writing a progress invoice: how it works – and how to avoid double VAT

Progress invoices secure your cash flow during long projects. How they work, when VAT becomes due and how to avoid the costly double taxation in the final invoice – explained clearly with an example.

Invoicing & Accounting

Invoicing & Accounting

Invoicing software 2026: GoBD- and e-invoice-ready, without accounting knowledge

What matters in invoicing software for 2026 – GoBD, e-invoicing, bookkeeping without prior knowledge – and how Easy Invoice in the PepperTools Office Cloud solves it: multilingual, mobile, hosted in Germany.