The ECB raises rates: what it really means for you as a small retailer (and what it doesn't)

Contents

- What the ECB decided

- What it means for your financing

- Does it affect Amazon prices?

- And the prices on Temu and AliExpress?

- The good news for your reserves

- What you can do now

- Conclusion

- Sources

Maybe you only caught it in passing: the European Central Bank (ECB) has raised interest rates. And this time it's more than routine – for the first time in almost three years, rates are going up again instead of down. After a long stretch of ever-cheaper money, that is a clear sign of a turnaround: the direction has reversed, and experts consider further steps possible.

Sounds like high politics, far from your own shop. But the honest question is: do you even notice it in your business? This article separates what matters from the noise – no politics lecture, just a clear look at your purchasing, your loans and your prices.

What the ECB decided

On 11 June 2026, the ECB raised its three key rates by 0.25 percentage points each (effective 17 June). The decisive one – the deposit rate – thus rose from 2.00% to 2.25%. What makes it special: it was the first rate hike since September 2023, ending a long phase in which money tended to get cheaper.

The reason is renewed inflation: in May it stood at 3.2% in the euro area instead of the targeted 2%, mainly due to higher energy prices following the Iran conflict. What matters for you is less the why than the signal behind it: the era of ever-cheaper money is over for now – experts even consider another small step this year possible.

What it means for your financing

This is the only point with a direct line to your account. When the key rate rises, banks usually pass higher rates on to variable-rate loans. Mainly affected:

- Overdraft / current-account credit on your business account – the most expensive item of all, on average around 11% and variable. Anyone permanently in the red here feels every hike.

- New working-capital or investment loans and leasing – fresh financing tends to get a bit more expensive.

Not affected are existing loans with a fixed rate – they stay as they are. Classic property financing also doesn't hang directly on the key rate, but on other market rates.

What does this mean for you? An example: an Etsy seller buys her seasonal supplies via the business overdraft and permanently carries 8,000 € there. At around 11% overdraft interest that's about 880 € a year – and exactly this rate can climb further with additional hikes. The lesson isn't „panic", but: don't let expensive variable credit become a permanent state.

Does it affect Amazon prices?

In short: no, not directly. Amazon prices arise from competition, demand and your own calculation – not from a 0.25-point ECB step. Anyone saying „because of the ECB everything on Amazon gets more expensive" is confusing cause and tool.

What really drives your purchase and sale prices is the inflation behind it: higher energy, material and logistics costs. These hit your margin harder than the rate decision itself. In other words: keep an eye on your purchase prices and margins – that's the real lever, not the key rate.

And the prices on Temu and AliExpress?

Here too the rate effect is negligible. The China platforms' prices depend on production costs in Asia, on shipping, on the dollar-euro exchange rate and – much more importantly – on the EU customs reform: from July 2026 a charge applies to small parcels.

And the exchange rate? It barely reacted to the hike: around the decision the euro continued to trade at about 1.15 US dollars, because the step had long been priced in. So a noticeable shift in Temu/AliExpress prices due to the ECB is not to be expected. If you want to know what really makes these providers more expensive, it's worth looking at the customs reform – we have a separate article on it: The 3-euro duty from July 2026: what online retailers need to know.

The good news for your reserves

There's also a flip side in your favour: rising key rates usually mean somewhat more interest on overnight and fixed-term deposits again. If you – as recommended – park your VAT reserve and a liquidity buffer separately, this money can now work a little more for you. Not wealth-building, but better than 0% on the business account.

What you can do now

Practical, no finance degree required:

- Check your overdraft. Is your business account permanently in the red? Then a cheaper, plannable working-capital loan is almost always cheaper than the overdraft.

- Clarify variable vs. fixed. Check on existing loans whether the rate is fixed or variable – only variable gets more expensive.

- Don't keep postponing planned investments. If further hikes come, it can make sense to lock in financing you've planned anyway at a fixed rate now.

- Keep an eye on liquidity. Punctual dunning keeps money in the house instead of bridging it expensively via the overdraft – see Dunning in 2026 for the self-employed.

- Park reserves with interest. VAT reserve and buffer on an overnight-deposit account rather than on the business account.

Conclusion

For a small retailer's day-to-day, the ECB rate hike is no drama, but a clear signal: money is no longer getting cheaper. It's directly noticeable only on variable financing – above all the expensive overdraft. Your Amazon, Temu or AliExpress prices, by contrast, don't hang on the rate decision, but on inflation, the exchange rate and the EU customs reform. Anyone who has their overdraft under control, sensibly secures planned investments and parks reserves with interest is on the safe side. For exactly this – liquidity overview, invoices and dunning – PepperTools supports you in day-to-day business.

Note: This article is general information and not individual financial or investment advice. For your specific situation, talk to your bank or an advisor you trust.

Sources

- ECB – Monetary policy decisions of 11 June 2026 — official statement on rates and rationale

- CNBC: ECB hikes interest rates for first time since 2023 — context on the first hike since 2023

- biallo: ECB raises key rate – what savers should do now — effects on loans and deposits

- finanzen.net: Euro slips against the dollar – ECB hike barely moves it — muted exchange-rate reaction

- Bundesbank: Development of corporate loans — background on rate pass-through to business loans

As of 14 June 2026. Rates and terms can change at short notice – the official ECB figures and your bank's terms are authoritative.

Handle invoices more easily

Easy Invoice combines quotes, invoices and customer management in the cloud.

Try Easy InvoiceRead next

Funding & Finance

Funding & Finance

Funding for Small Businesses 2026: The Most Important Grants and Loans at a Glance

Grants you don't repay, low-interest development loans and tax breaks – sorted by type and each with a link to the official body. So you can see what really fits your business.

Funding & Finance

Funding & Finance

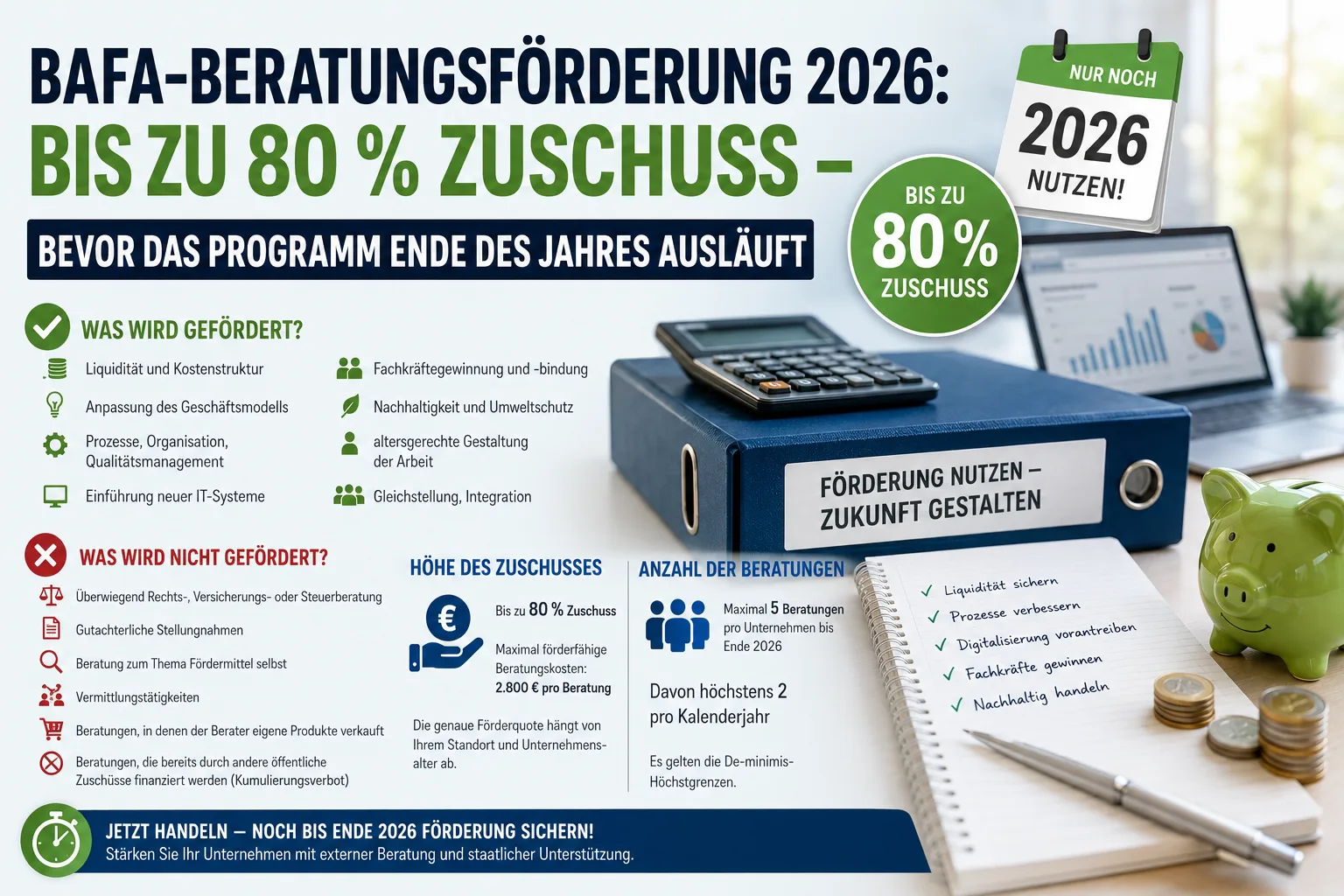

BAFA Consulting Grant 2026: Up to 80 % Subsidy in Germany

Germany's BAFA consulting grant ends in December 2026. Up to 80 % subsidy for external business consulting — who can apply, what's funded, and the mistake that voids the grant.

Funding & Finance

Funding & Finance

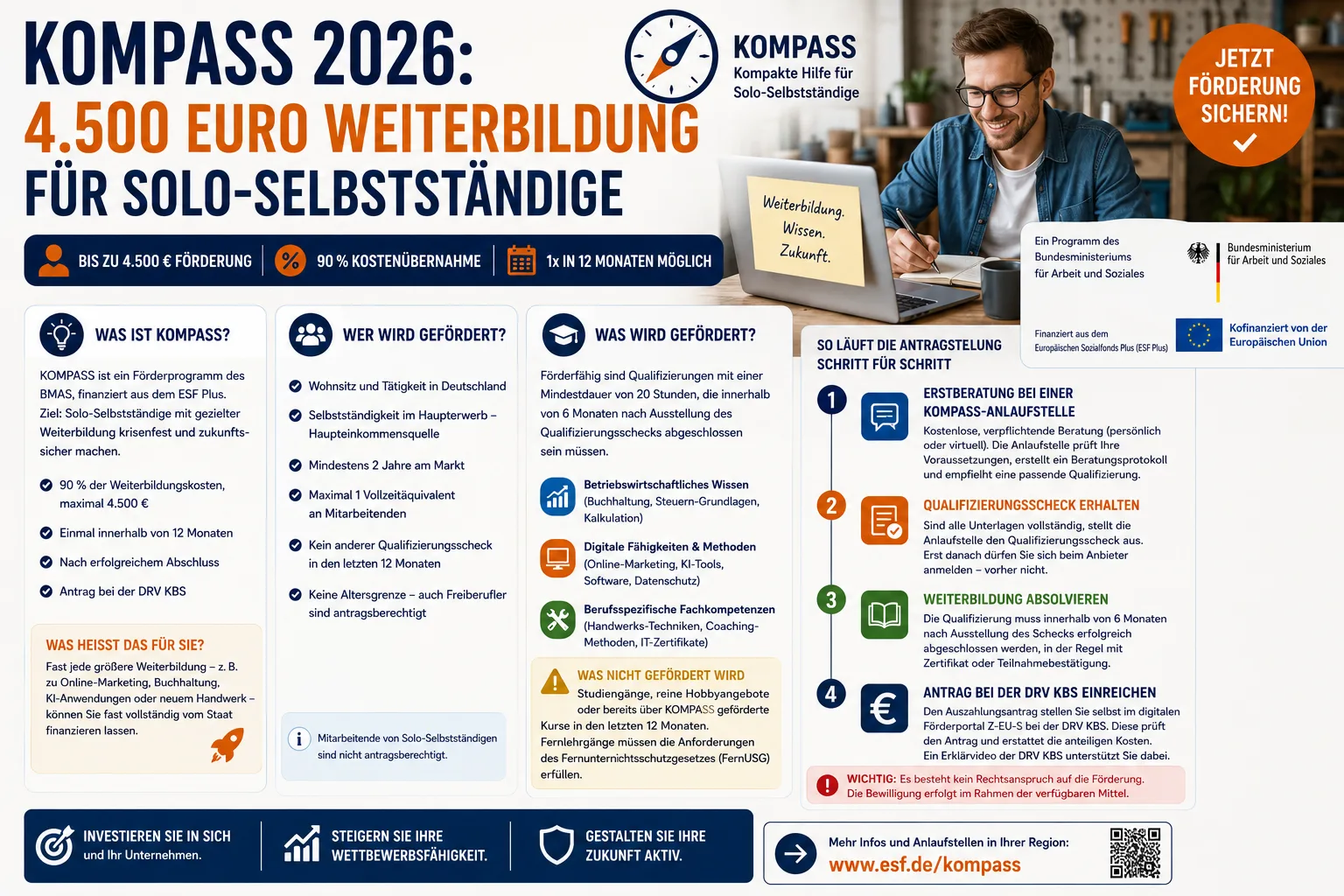

KOMPASS 2026: €4,500 Training Subsidy for Solo Entrepreneurs

Solo entrepreneurs in Germany can get up to €4,500 reimbursed for training through KOMPASS. With the May–October 2026 voucher cap, here is how to apply smartly.